Laura McKenzie/Texas A&M AgriLife Marketing and Communications

Check how the USDA Livestock Risk Protection (LRP) program can help you lock in profits and manage price risk; whether you are running a large ranch operation or just a few head.

How Can We Use LRP in Today’s Market?

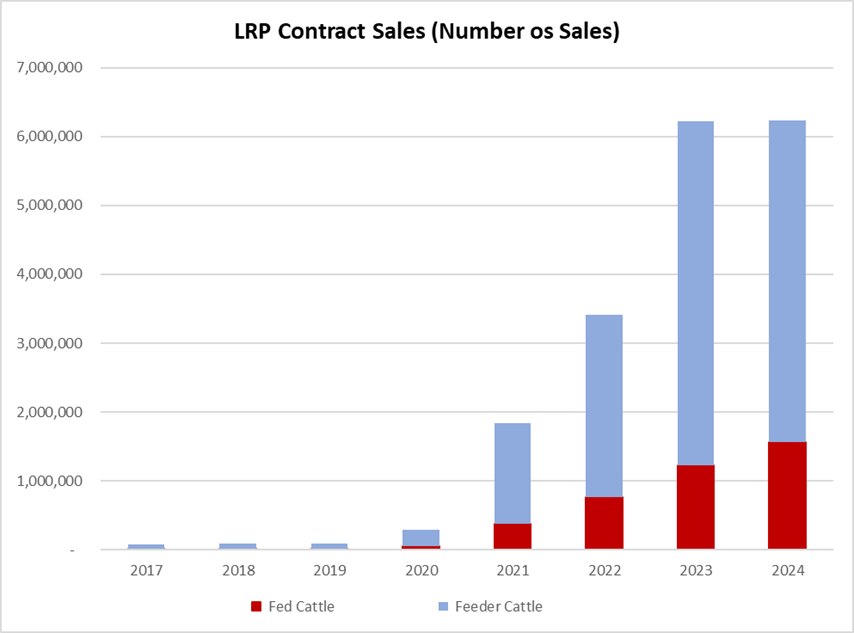

Producers across the United States are increasingly adopting the Livestock Risk Protection Program, commonly known as the LRP. This program was designed to protect ranchers against falling cattle prices. From a mere 71 thousand heads covered in 2017, the usage of LRP has increased rapidly to 6.2 million heads by 2024 (Figure 1). This increase aligns with the changes to the LRP program done by the USDA and the significant improvement in the market feeder and live cattle prices.

Figure 1: LRP Usage

During the summers of 2019 and 2021, the USDA introduced several modifications to the LRP program. These changes reduced the premiums paid by ranchers and allowed them to defer premium payments until the end of the endorsement period, making it accessible across all states and counties. The option to pay premiums at the program’s period offers ranchers a considerable cash-flow advantage compared to purchasing Put Options in the futures market.

The rise in cattle prices has also emphasized the importance of implementing a solid price risk management plan. The LRP helps minimize financial losses, secure profit margins, and reduce the risk of business failure, particularly in the face of higher investment levels. The increased adoption of LRP reflects a growing number of ranchers who have included risk management plans to protect their operations. These ranchers significantly reduce the threat of business failure by setting a floor price for their cattle.

Another benefit of the LRP program is its accessibility. It doesn’t require a minimum number of cattle to be insured, meaning even small ranchers with just one cow can take advantage of its benefits. Most importantly, cow-calf and stocker operations can LRP to protect their prices.

Although LRP premiums are often cheaper compared to Put Options due to the level of subsidy, premium costs depend on the expected end price, the coverage level, and the endorsement length. One disadvantage of operating with LRP is that once you purchase the insurance, there is no option to offset that position at any time, as we might be used to operating options in the future market.

Example: June 2024 Stockers

While cow-calf margins remain strong, margins for stockers and feedyards have tightened over the past year. In this environment, it is crucial to explore all risk management options available. Understanding both cash and accrual costs is essential before selecting a coverage level, as this helps determine the appropriate price to hedge.

You can choose to hedge for:

- Full price – Lock in your total expected profit margin

- Total cost breakeven price – Cover all economic costs, including depreciation and unpaid labor

- Cash flow breakeven price – Cover just your cash expenses to mitigate short-term loss exposure.

Using the Capital Farm Credit Premium Quoter Tool, we estimated Livestock Risk Protection (LRP) costs for stockers weighing 800 lbs. each, scheduled for sale in late June 2024.

Table 3. LRP Example for June 2025 Stockers

At a 100% coverage level, the program’s target price is $288.95 per CWT, with a net producer’s premium after the subsidy of $7.42 per CWT. This results in a total premium per head of $59.36. At a 95% coverage level, we guarantee a net price of $265.38 per CWT, with total premium costs of $26.08 per head. If the USDA’s reported price falls below your coverage price, you will receive an indemnity payment. Conversely, if the market price exceeds your insured price, you will not receive a payment, but you will still benefit from a higher market price.

Final Thoughts

Similar LRP strategies can be applied to fed cattle, depending on your target sale month. Regardless of how you plan to use LRP, the key to effective hedging is to know your breakeven prices and to set realistic target margins.

For further information on LRP, please refer to the USDA Fact Sheet (Livestock Risk Protection Fed Cattle | RMA (usda.gov)). The USDA website lists approved livestock agents and insurance companies if you want to buy the insurance.

On this example I have use the Capital Farm Credit LRP insurance tool. For more information about if please contact your local Capital Farm Credit office.