Field crops in Burleson County on July 30, 2021. (Laura McKenzie/Texas A&M AgriLife Marketing and Communications)

On May 10, USDA released a new World Agriculture Supply and Demand Estimate (WASDE) report. In this week’s post, we’ll look at what the report has to say about cotton and grain crop production in the 2024/25 crop year.

Overview

The May WASDE report is always an important one for producers and analysts because it contains USDA’s first official projects for production and use in the new crop year. In this year’s report, USDA takes projections for winter wheat production from the May 10 Crop Production report. For other crops, projections for planted acreage are based on the March 28 Prospective Plantings report. Projections for harvested acreage and yield use historical trends as their basis. In general, the expectation this year is for increased supplies and ending stocks relative to last year.

Wheat

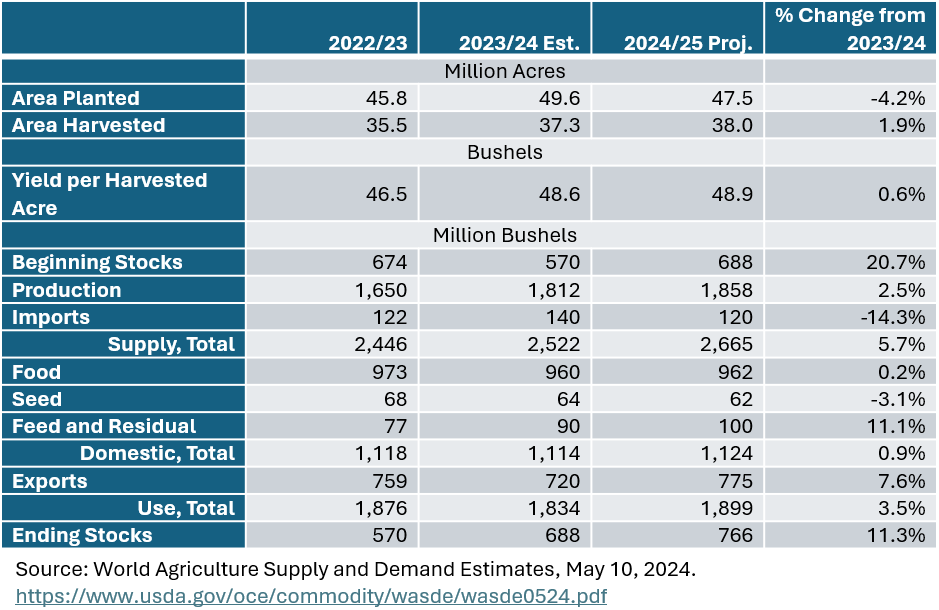

U.S wheat production is expected to be 1,858 million bushels this year (Table 1). This is a 2.5% increase relative to the 2023/24 crop year, driven by an increase in acres harvested and yield per harvested acre. Total supplies in 2024/25 are projected to increase by 5.7% because of both increased carryover from last year’s crop and increased production this year. Wheat use in 2024/25 is projected at 1,899 million bushels, a 3.5% increase relative to 2023/24. As a result, ending wheat stocks are also expected to increase by 78 million bushels.

The global outlook for wheat production is for increased production and total use this year. However, smaller worldwide carryover from the 2023/24 crop should result in a small decrease in total supplies and ending stocks.

Table 1. WASDE Wheat Supply and Demand

Corn & Sorghum

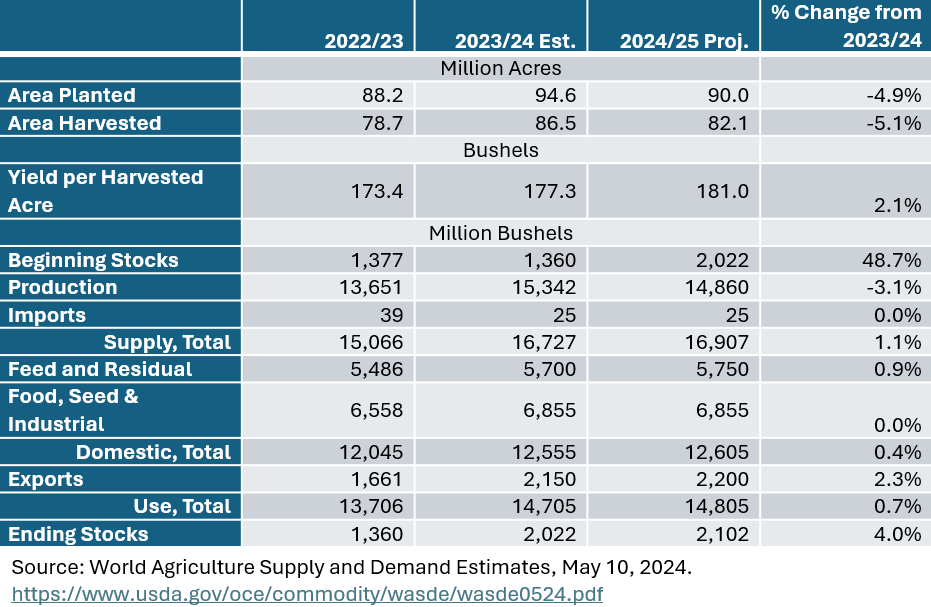

For corn, the May WASDE projects production in the U.S. to decrease by almost 500,000 bushels despite potential record-high yields (Table 2). Still, with carryover from the 2023-24 crop factored in, total corn supplies are expected to increase slightly this year relative to last year. The use side of the corn balance sheet should remain stable relative to last year. The report shows a small 100,000 bushel increase in total use this year, driven largely by an increase in corn exports. As a result, ending stocks this year are expected to increase by about 80,000 bushels.

In terms of the global outlook, the report projects a very small decrease in corn production worldwide along with a very small increase in use. The result is a 0.8 metric ton expected decrease in world corn ending stocks.

Table 2. WASDE Corn Supply and Demand

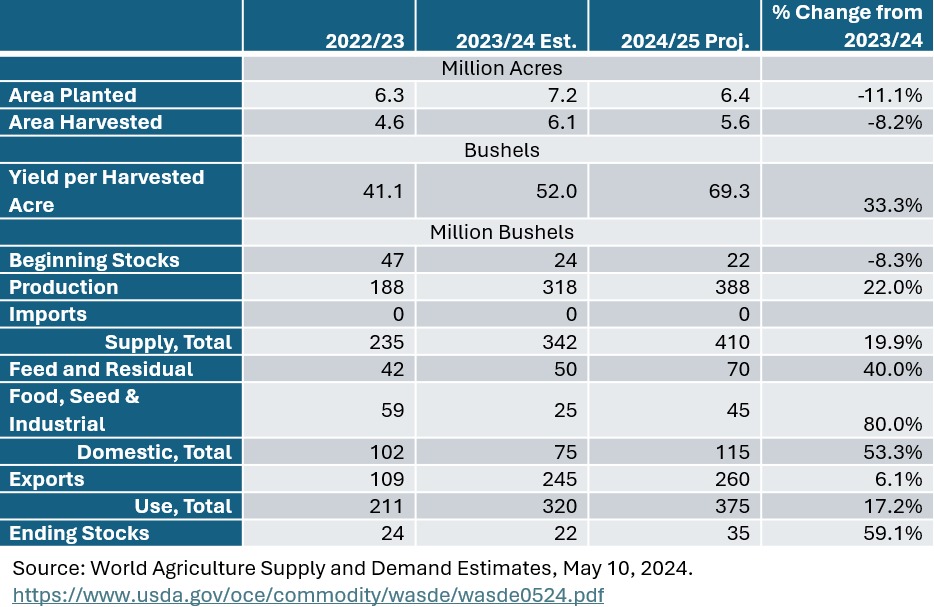

The domestic outlook for sorghum calls for increased production, use, and ending stocks Table 3. Production increases because of greater yield per harvested acre outweighing fewer acres planted and harvested. Sorghum use increases in every category, but not enough to equal production increases. Ending stocks are expected to increase by 13 million bushels.

Table 3. WASDE Sorghum Supply and Demand

Cotton

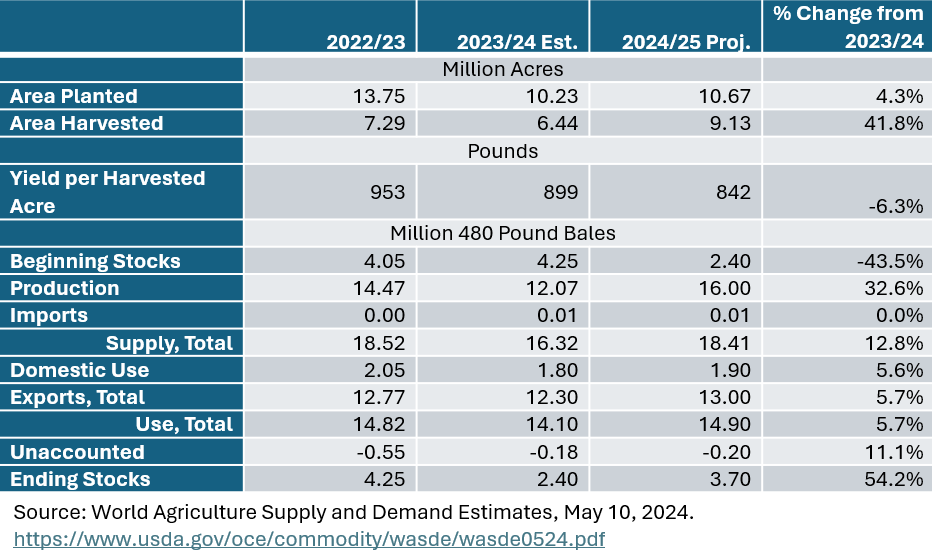

The May WASDE report for U.S. cotton projects large increases for production and ending stocks, along with a small increase in use (Table 4). Production is expected to increase from 12 million bales in the 2023/24 crop year to 16 million bales this year. However, this projection is contingent upon favorable growing conditions and abandonment that is in line with the historical average. Although production is projected to increase by 4 million bales, carryover from the 2023/24 crop is small. So, total supplies are expected to increase by only 2 million bales relative to last year. While the report also predicts a 700,000-bale increase in exports, and an 800,000-bale increase in total use, this is not enough to keep up with the increase in production. Ending stocks for 2024/25 are expected to increase to 3.7 million bales.

World cotton production is expected to increase this year by about 5.5 million bales. Use is only expected to increase by 3.5 million bales. Global ending stocks are projected to increase this year by 2.5 million bales.

Table 4. WASDE Cotton Supply and Demand

Takeaways

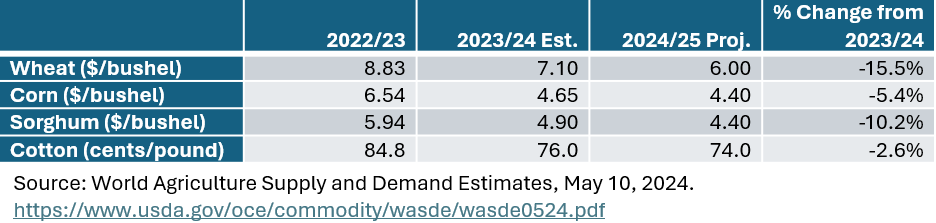

The trend in the May WASDE for the 2024/25 crop year is large increases in supplies relative to use. As a result, the May WASDE projects season average farm prices for wheat, corn, sorghum, cotton to decrease during the 2024/25 crop year (Table 5). This does not mean that there will not be marketing opportunities this year. Make sure to review your marketing plan and make any changes you think are necessary to take advantage of those opportunities as they come.

Also, keep in mind that the May WASDE represents early projections for corn, sorghum, and cotton production. We’re still a long way from being able to define production levels for these crops with any certainty. Use these estimates as a baseline for your expectations but be prepared for them to change through the summer.

Table 5. WASDE Season Average Farm Prices for wheat, corn, sorghum, and cotton